Nicholas Anthony

Central bankers have promised everything when it comes to central bank digital currency (CBDC). One would hope they would realize just how outlandish it is to say a CBDC can do everything, everywhere, all at once if they just took a moment to review their promises. However, these are busy times.

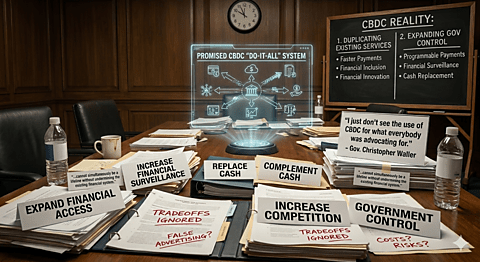

So, let’s briefly look at everything that has been promised. Across speeches, reports, and proposals, policymakers have claimed that a CBDC will:

Expand financial access to the unbanked.

Improve the application of monetary policy.

Increase the speed of payments.

Improve cross-border payments.

Increase competition.

Increase financial system resilience.

Enhance financial stability.

Create programmable payments.

Increase financial surveillance.

Evade sanctions.

Enhance government payments.

Enhance the digital transformation of the economy.

Strengthen the international role of currencies.

Prevent the use of cryptocurrency.

Prevent dependency on foreign payment services.

Establish universal acceptance.

Compete with private services while also not competing with all private services.

Replace cash while also complementing cash.

Create a free option for consumers while still paying businesses’ fees.

“Future-proof” the economy.

Reduce currency fragmentation.

Reduce costs for businesses and consumers.

Create a foundation for financial innovation.

Prevent discrimination against central bank money.

At best, this list showcases extreme optimism in the efficacy of government programs. At worst, this list borders on false advertising. More importantly, many of these goals pull in different directions, requiring tradeoffs that policymakers often gloss over. A system designed to maximize surveillance, for example, is not easily reconciled with one meant to expand financial inclusion. Likewise, a CBDC cannot simultaneously be a lifeline without undermining the existing financial system. And that’s to say nothing of the fact that these officials almost never address the risks of CBDCs.

Perhaps my skepticism is the foil to their optimism, but I’m not alone. Federal Reserve Governor Christopher Waller recently addressed CBDC proponents head-on:

I just don’t see the use of CBDC for what everybody was advocating for. … What is the major problem this thing is solving? And why is a CBDC and only a CBDC the answer to fixing that problem? … So once you ask that basic question and you realize everything works pretty well without it. There’s no reason to spend a lot of money on it.

It’s not often that I commend central bankers, but Waller is spot on. A CBDC can’t do everything, everywhere, all at once. In fact, what little it can do seems to fall into just two categories: duplicating existing services (e.g., faster payments, financial inclusion, and financial innovation) and expanding government control (e.g., payment programmability, financial surveillance, and cash replacement). If that’s the best that officials can come up with, CBDCs should be rejected.